Securing the cash for a commercial property isn't just a simple transaction; it's a strategic process that blends the right loan, solid financials, and a strong relationship with your lender. Getting this right is critical, especially in a market where interest rates and what lenders expect can change on a dime. Let’s map out the journey ahead and get you grounded in the essentials.

Your First Look at Commercial Property Financing

Right off the bat, you need to know that financing a commercial property is a completely different ballgame than getting a home mortgage. Lenders aren't just looking at your personal credit score. They’re laser-focused on one thing: the property's ability to generate income.

This means you should prepare for a much deeper dive into your business's financial health and the building's potential to be profitable. Understanding this is key, particularly with the way the economy is shaping up. Many property owners are hitting a wall trying to refinance because interest rates are higher and lending standards are way tighter than they were a few years ago.

Your first step should be to explore the wide world of commercial property financing options, from traditional bank loans to more creative solutions.

The Current Market Landscape

The commercial real estate market is definitely feeling the pressure right now. In 2025, an estimated $957 billion in commercial real estate loans are coming due—a figure that’s nearly triple the 20-year average. This "maturity wall" is forcing a ton of borrowers to refinance in a really tough environment.

To make matters worse, delinquency rates for some loan types, like those bundled into commercial mortgage-backed securities (CMBS), have shot up to 7.29%. That's a clear signal of distress in the market.

To get through this, you'll need more than just a good credit score. You need a rock-solid strategy, a clear-eyed view of your project's costs, and a story that convinces a lender your project is a winner.

This guide is designed to give you that strategic edge. We'll walk you through every step so you're ready to make a strong case to any lender. Here’s a sneak peek at what we’ll cover:

- Loan Types: We’ll break down the best financing vehicles for steel buildings, from conventional and SBA loans to bridge financing.

- Lender Expectations: I’ll pull back the curtain on what underwriters really care about, like your debt service coverage ratio (DSCR).

- Application Process: We'll go over how to assemble a professional loan package that actually gets you noticed.

Whether you're buying your first warehouse or adding a new metal building to your portfolio, the numbers have to make sense. Before you even think about talking to a lender, it’s smart to get a firm handle on the estimated commercial metal building cost. This ensures your financing request is realistic and backed by solid data from the get-go.

Finding the Right Commercial Property Loan

Securing the right financing for a commercial building isn't about finding the "best" loan out there. It's about finding the best fit for your specific project. A loan that’s perfect for a stable, fully-leased office complex is almost certainly the wrong choice for a fixer-upper warehouse you plan to renovate.

Understanding the lending landscape is key. Right now, it’s not just about interest rates. With economic uncertainty and high construction costs, lenders are taking a much closer look at new projects. Let's walk through the most common financing routes to see where your deal fits.

Traditional Bank and Credit Union Loans

For most borrowers with solid credit and a proven track record, a conventional loan from a local bank or credit union is the default choice. These institutions know their local market inside and out, which often translates to competitive rates and fair terms, usually between 5 to 20 years.

But here's the catch: they're conservative. Banks want to see a predictable, income-generating property. If you're buying a brand-new building that hasn't proven itself or a property that needs a ton of work, a traditional lender will likely pump the brakes. They're in the business of minimizing risk, not gambling on potential.

Government-Backed SBA Loans

The Small Business Administration (SBA) has a couple of powerhouse programs that can be a lifesaver, especially if you're a business owner buying a property for your own company to use.

- SBA 7(a) Loan: This is the SBA’s flagship program. You can use it for just about any business need, including buying real estate. The government guarantees a big chunk of the loan, making banks feel much safer and often leading to better terms for you.

- SBA 504 Loan: This one is specifically for buying major assets like buildings or heavy equipment. The biggest selling point? You might only need 10% down. The loan is split between a bank (50%), a Certified Development Company (40%), and you (10%), making it incredibly accessible.

Key Insight: There’s one major rule for both SBA loan types: your business has to occupy at least 51% of the building. This makes them perfect for owner-users, but they won't work for passive real estate investors.

To help you compare, here's a quick breakdown of the most common commercial financing options.

A Quick Look at Commercial Loan Options

| Loan Type | Best For | Typical LTV | Pros | Cons |

|---|---|---|---|---|

| Traditional Bank Loan | Established businesses with strong credit buying stable, income-producing properties. | 65%–80% | Competitive rates, long terms. | Strict requirements, slow approval process. |

| SBA 7(a) Loan | Owner-occupied commercial real estate and general business purposes. | Up to 90% | High LTV, flexible use of funds. | Requires business to occupy 51%+ of the space. |

| SBA 504 Loan | Major asset purchases, like buildings and equipment, for owner-occupiers. | Up to 90% | Very low down payment, fixed rates on CDC portion. | Complex structure, strict use-of-funds rules. |

| Hard Money Loan | Short-term financing for quick acquisitions or properties needing renovation. | 60%–75% | Very fast funding, based on asset value not credit. | High interest rates and fees. |

| Bridge Loan | "Bridging" the gap until long-term financing is secured for time-sensitive deals. | 70%–80% | Fast closing, flexible terms. | Short-term solution with higher costs. |

Each of these loan types serves a distinct purpose. The key is matching the loan's strengths to your project's specific needs and timeline.

Alternative and Private Financing

So, what happens if your deal is a little outside the box and banks won't touch it? That’s where alternative lenders step in. These options are usually faster and more flexible, but that convenience comes at a higher cost.

A hard money loan, for instance, is a short-term loan based on the property’s value, not your personal credit score. An investor might use one to snap up a property quickly, fix it up, and then refinance into a traditional loan once the property is stabilized and generating income. For a deeper dive, this comprehensive guide to property investment loans is a great resource.

Bridge loans work in a similar way, "bridging" a gap in funding until you can lock in a permanent loan. They're ideal for situations where you need to close fast or for properties that need some work before they can qualify for bank financing. If your project involves a specific structure, it's also smart to look into financing options tailored for different types of commercial steel buildings to find the best possible solution.

What Lenders Really Want to See

To get your commercial building financed, you need to switch gears. Stop thinking like a buyer and start thinking like a bank underwriter. Lenders are naturally risk-averse—their main job is to make sure every loan they issue gets paid back, on time, without fail. This means they’re going to put both you and the property under a microscope.

While your personal credit score and business history are definitely the first things they'll look at, that's just the start of the conversation. Lenders need to see that you have some real skin in the game. That means having plenty of cash reserves on hand for the down payment, closing costs, and a buffer for those inevitable surprises. If you have any experience managing commercial real estate, make sure you highlight it. It tells them you know what you’re getting into.

Decoding the Key Ratios

Beyond your personal financials, underwriters live and breathe by two critical numbers: the Loan-to-Value (LTV) ratio and the Debt Service Coverage Ratio (DSCR). These ratios give them a clear, black-and-white picture of the deal's risk level.

Loan-to-Value (LTV) simply compares the loan amount to the property’s appraised value. Let's say you're after a $750,000 loan for a building appraised at $1,000,000. Your LTV would be 75%. Most lenders will cap commercial LTVs somewhere between 65% and 80%, which means you should plan on a down payment of at least 20% to 35%. A lower LTV is always better, as it shows the lender you have more equity at stake.

The All-Important DSCR

If there's one metric that can make or break your loan application, it's the Debt Service Coverage Ratio (DSCR). This number directly measures if the property can generate enough cash to cover its own mortgage payments. Lenders aren't looking for you to just break even—they need to see a healthy cushion.

The formula is pretty straightforward:

DSCR = Net Operating Income (NOI) / Total Debt Service

- Net Operating Income (NOI) is your total income from the property (rent, fees, etc.) minus all your operating expenses (taxes, insurance, maintenance).

- Total Debt Service is the sum of all your principal and interest payments for the year.

Most lenders won't even look at a deal with a DSCR below 1.25x. This means for every $1.00 you owe in annual mortgage payments, the property needs to bring in $1.25 in net income. Anything under 1.20x is a huge red flag, but if you can show a DSCR of 1.40x or higher, you'll look like a rockstar borrower.

Let's walk through a real-world scenario for financing a pre-engineered steel building warehouse.

Example Calculation

Imagine you want to buy a steel warehouse that you project will generate $100,000 in Net Operating Income (NOI) each year. The total annual mortgage payment for the loan you’re seeking comes out to $80,000.

- DSCR = $100,000 (NOI) / $80,000 (Debt Service) = 1.25x

You’ve hit the lender's minimum target exactly. As long as your personal credit and LTV check out, this deal has a strong chance of getting approved. But if your NOI was just a bit lower—say, $90,000—your DSCR would drop to 1.125x, and that loan application would almost certainly be denied. This is why properly projecting the income potential of different structures is so crucial. Getting familiar with the specifics of a steel building warehouse can help you build a financial forecast that lenders will feel confident in.

Building Your Commercial Loan Application Package

Putting together a sharp, complete loan package is about more than just checking boxes. It’s the first real impression a lender will have of you. Think of it this way: an underwriter's job is to poke holes in your story. Your job is to hand them a story so solid and well-supported that there are simply no holes to be found.

Your application really tells two stories at once: one about you as a trustworthy borrower, and another about the property as a smart investment. You have to nail both.

Assembling Your Personal and Business Documents

First things first, lenders need to know who they're dealing with. This part of the package is all about proving you're a reliable operator with the financial footing to see this project through. Don't just collect the paperwork; look at it through a lender's eyes to catch any potential red flags before they do.

Typically, you'll need to pull together:

- Personal and Business Tax Returns: Lenders will want to see the last two to three years to verify your income and financial history.

- Personal Financial Statement (PFS): This is a detailed snapshot of your assets, liabilities, and overall net worth. Be honest and thorough here.

- Business Operating Agreement and Formation Documents: Your LLC or incorporation documents that prove your business is legitimate and in good standing.

- Resume or Bio: This is especially important if you're newer to real estate. Use it to highlight any relevant management, business, or property experience you have.

Detailing the Property's Financial Story

Once you've established your own credibility, the spotlight shifts to the building itself. These documents need to paint a crystal-clear picture of the property's financial health and its potential for profit. This is where you prove the investment makes sense on its own.

The key property-specific documents you’ll need are:

- Executed Purchase and Sale Agreement: The fully signed contract to buy the property.

- Rent Roll: A detailed list of every current tenant, their lease terms, what they pay, and their security deposits. Lenders live in this document, looking at tenant quality and when leases are up for renewal.

- Trailing 12-Month Operating Statement (T-12): This shows the property's real-world income and expenses over the past year. No guesswork here, just facts.

- Pro Forma Statement: This is your projection of the property’s future income and expenses under your management. It needs to be optimistic but grounded in reality—be ready to defend every assumption you make.

Pro Tip: Don't just dump a pile of documents on a lender's desk. Create a clean, one-page Executive Summary and put it right on top. Briefly introduce yourself, describe the property, highlight the deal's strengths (like a strong DSCR or a high-quality tenant), and clearly state your loan request. It’s your chance to shape the narrative from the very beginning.

When you're pulling these documents together, especially the pro forma, having a deep understanding of the property type is a massive advantage. Our guide to buying a metal building can give you the kind of specific insights that help create financial projections that a lender will actually believe.

Navigating the Loan Process from Start to Finish

Once your loan package is in the lender's hands, the real waiting game begins. Understanding the journey from application to closing day helps demystify the process and lets you know what to expect next. This isn't just a simple checklist; it's a dynamic phase where good communication and being prepared are your best assets.

First up is the initial review. A loan officer or analyst will give your package a once-over to make sure all the necessary documents are there and that the deal fits their basic lending criteria. If you pass this initial sniff test, you’ll probably get a term sheet or a Letter of Intent (LOI). Think of this as the lender’s way of saying they’re serious. This non-binding document will outline the proposed loan amount, interest rate, and other key conditions.

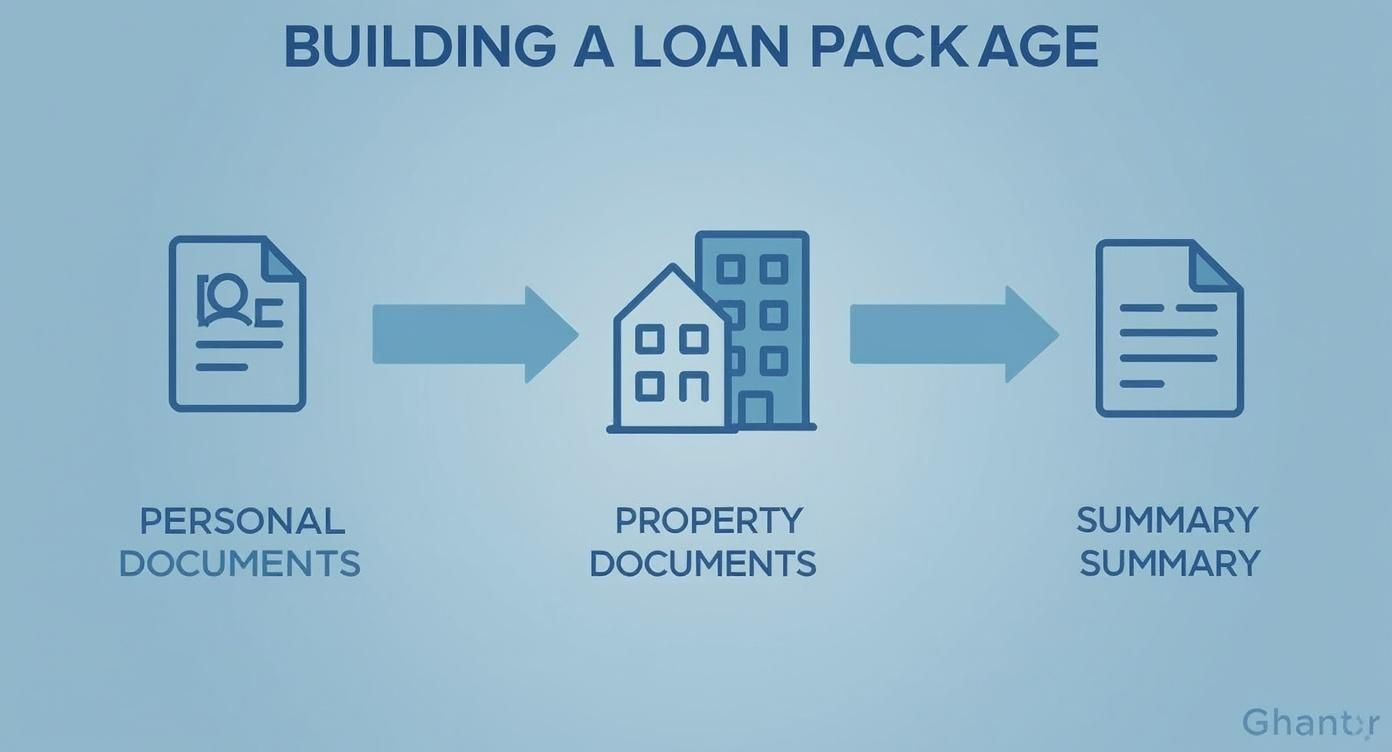

This infographic gives you a simple visual of the core pieces needed to build a strong loan application.

As you can see, the three pillars—personal, property, and summary documents—all have to work together to tell a compelling story to the lender.

Entering the Due Diligence Phase

After you accept the term sheet, things get real. You're now in the critical due diligence period. This is where the lender starts spending their own money to verify everything you've claimed. The two biggest hurdles here are the appraisal and the environmental report.

- The Appraisal: An independent, third-party appraiser is hired to figure out the property's real market value. If the appraisal comes in lower than your purchase price, it can throw a wrench in the whole deal by messing up the loan-to-value (LTV) ratio.

- Environmental Reports: A Phase I Environmental Site Assessment (ESA) is pretty much standard. This report digs into the property's history to check for any potential contamination issues that could become a liability for the lender down the road.

While this is happening, the formal underwriting process kicks off. An underwriter—the ultimate decision-maker—will meticulously comb through every single document, double-check your financials, and stress-test your projections. They will almost certainly come back with questions, so be ready to give clear, quick answers to keep the ball rolling.

From Commitment to Closing

If the underwriter likes what they see, they’ll issue a formal loan commitment. This is the official "yes" you've been waiting for. It’s a legally binding agreement from the lender to fund your loan, as long as all the final conditions are met. From here, your file is handed off to the closing department, where attorneys will draft the final loan documents for you to sign.

The good news is that the financing landscape for commercial property seems to be getting better. According to the Federal Reserve Senior Loan Officer Opinion Survey, by June 2025, only 9% of banks reported tightening their commercial real estate loan standards. That's a huge drop from 67.4% back in April 2023. This shift suggests that lenders are regaining confidence, which can only help smooth out the underwriting process for qualified borrowers.

This whole process can feel long and complicated, but staying organized makes a world of difference. To get a head start and see what lenders will ask for, check out our resources to get financing for your steel building project.

Common Questions on Commercial Property Financing

Even after you nail down the big picture, you're bound to run into specific questions when financing a commercial building. Getting straight answers to these common roadblocks will save you a ton of time and keep you from making costly missteps. Let's dig into some of the most frequent questions we hear from borrowers.

How Much of a Down Payment Do I Need for Commercial Property?

You’ll definitely need to bring more cash to the closing table than you would for a typical home purchase. Most commercial lenders are looking for a down payment somewhere in the 20% to 35% range.

The exact number really depends on the risk level of the deal. For instance, a lender might feel comfortable with a 20% down payment for a stable, fully-leased office building with a well-known anchor tenant. But for something they see as riskier, like a new hotel or a speculative construction project, they might ask for as much as 35% down to buffer their risk.

That said, there are some great exceptions. The SBA 504 loan program is a real game-changer for business owners buying property for their own company, often letting them get in the door with a down payment as low as 10%.

Can I Use a Commercial Loan to Finance a Mixed-Use Property?

Absolutely. Financing mixed-use properties is pretty common, and lenders have a clear process for it. They'll underwrite the loan by looking at the income coming from both the commercial and residential parts of the building.

The underwriter will take a hard look at the financial strength and lease terms of your business tenants and compare that to the stability and market rates of your residential renters. Here's a key tip: if your own business will occupy more than half of the space—51% or more—you could qualify for some very appealing owner-occupied financing, like an SBA loan. Those usually come with much better terms and a lower down payment.

What Is a Prepayment Penalty and How Does It Work?

A prepayment penalty is a fee the lender hits you with if you pay off your loan early. It’s a common feature in long-term, fixed-rate loans (especially CMBS "conduit" loans) because it protects the lender's expected profit on the interest.

A hefty prepayment penalty can essentially lock you into a loan, making it financially impossible to sell or refinance when you want to. You have to scrutinize this clause before signing anything.

The two most common types are "yield maintenance" and "defeasance." They’re both complicated, but their goal is the same: to make you pay the lender for the interest income they’ll lose because you paid off the loan ahead of schedule. Understanding this term is critical, as a nasty penalty can completely derail your investment strategy and limit your flexibility down the road.

At Icon Steel Buildings, we provide durable and customizable metal buildings perfect for any commercial venture. Our structures are designed to offer long-term value, making your financing journey smoother by presenting a solid, reliable asset to lenders. Find out how our American-made steel buildings can be the foundation of your next successful project by visiting us at https://iconsteelbuildings.com.